Key Findings

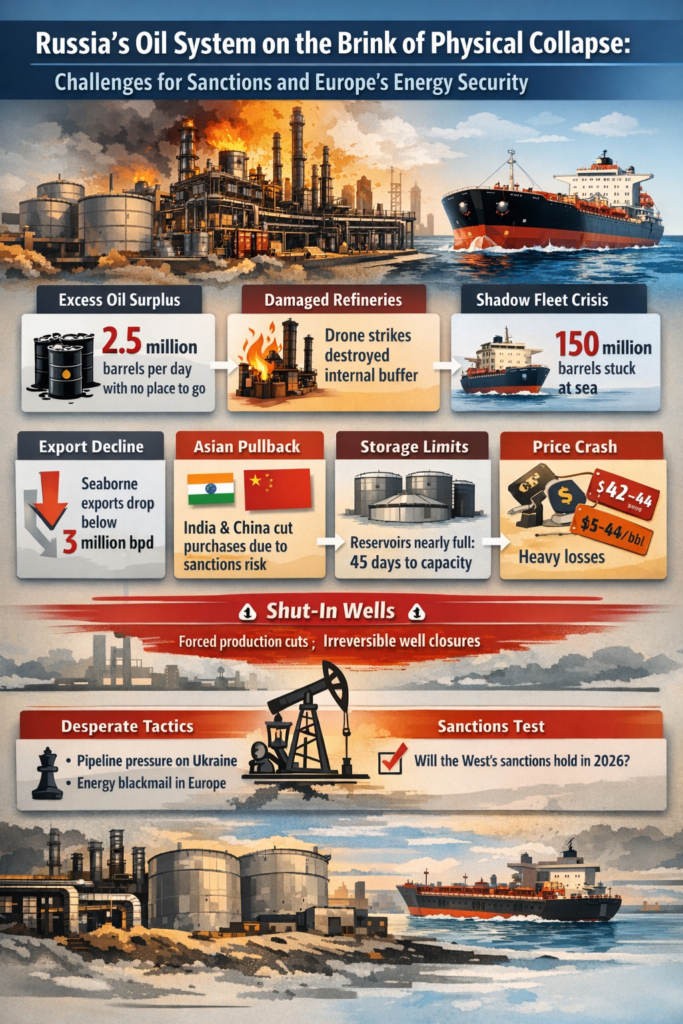

- Russia’s oil sector has entered a phase of physical crisis, where the main constraints are no longer prices but storage and transportation capacity.

- A decline in seaborne exports below 3 million barrels per day, combined with production of around 9 million barrels per day, has created a daily surplus of approximately 2.5 million barrels that Russia can neither refine domestically nor safely store.

- Drone attacks on refineries have eliminated Russia’s internal absorption buffer for excess crude.

- Russian oil companies have already begun forced production cuts, which may become systemic by spring 2026.

- The so-called “shadow fleet” has shifted from a sanctions-evasion tool into a capital freeze mechanism, with roughly 150 million barrels stranded at sea.

- India and China, fearing secondary sanctions, have sharply reduced purchases, depriving Moscow of its key Asian markets.

- Limited onshore storage capacity leaves Russia with less than two months before it completely loses the ability to ship new oil.

- The collapse of Urals crude prices and rising logistics costs are destroying the profitability of complex fields.

- Technological characteristics of Russian oil wells make large-scale shut-ins partially irreversible.

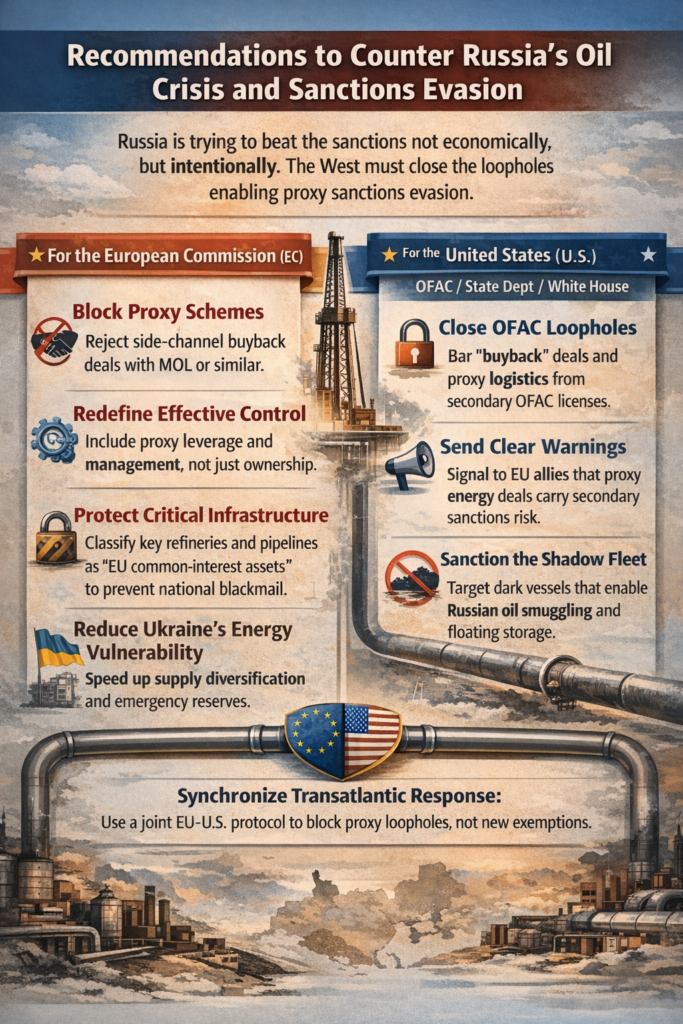

- In response, the Kremlin is shifting from economic tools to political coercion, attempting to manufacture artificial demand in Europe.

- The NIS case, pressure on the Druzhba pipeline, and energy blackmail of Ukraine are elements of a single strategy.

- The success or failure of these schemes will test the resilience of the Western sanctions architecture in 2026.

Systemic Breakdown Dynamics

Russia’s oil industry faces the risk of a technical shutdown by mid-spring 2026 due to critical saturation of all available storage infrastructure and the inability to rapidly reroute exports after the withdrawal of key buyers. This will force the Kremlin to make decisions on mandatory well shut-ins under unfavorable conservation conditions, jeopardizing future production recovery.

Total seaborne crude shipments from Russian ports have fallen from 4 million to less than 3 million barrels per day. With stable production near 9 million barrels per day, this creates a daily excess of 2.5 million barrels, which cannot be refined domestically due to refinery capacity losses from drone attacks. Because surplus oil cannot be stored technologically, Russian companies have already implemented forced production cuts of 130,000 bpd in December–January, with forecasts indicating declines of up to 300,000 bpd by March–April 2026 as Transneft’s pipeline system and storage facilities overflow.

Under U.S. pressure, India reduced Russian oil imports from an annual average of 1.7 million bpd to 1.1 million bpd in January, with further declines to 800,000 bpd projected for March, representing a loss of over 50% of the Indian market in just three months.

As of February 2026, approximately 150 million barrels of Russian oil worth $6.4 billion remain stranded on shadow fleet tankers due to refusals by Indian and Chinese state companies to accept new cargoes amid heightened secondary sanctions scrutiny. This volume equals nearly two months of Russia’s total seaborne export capacity, with an additional 1 million barrels per day continuing to accumulate onboard tankers functioning as floating storage.

Russia’s onshore storage capacity, estimated at 32 million barrels, is already 51% full. Combined with the limited availability of the shadow fleet, this leaves Russia with approximately 45 days before it becomes physically impossible to ship additional oil under a worst-case scenario.

The price of Urals crude at Baltic ports (Primorsk and Ust-Luga) has dropped to $42–44 per barrel, creating a record discount of over $28 versus Brent, effectively eliminating profitability at complex fields. In January 2026, 47% of Russia’s seaborne oil exports were carried by sanctioned tankers, raising logistics and insurance costs by $15–20 per barrel.

Federal budget revenues from the oil and gas sector fell to $4.3 billion (393 billion rubles) in January 2026, the lowest level since the pandemic and only half of the previous year’s intake. This creates an additional annual budget shortfall exceeding $20 billion from this sector alone.

The technological specificity of Russian oil fields prevents painless conservation: halting oil flow leads to paraffin solidification and reservoir pressure loss, making 50–70% of shut-in wells unrecoverable without major capital investment.

The rapid degradation of the oil services sector, with drilling rates down 16% in December, signals the exhaustion of Western equipment stockpiles and the inability to sustain mature fields that require constant well renewal. Within 1–2 years, depletion will no longer be offset by new capacity, triggering an irreversible decline in oil revenues regardless of global prices.

The Russian government has officially banned publication of production and export statistics until April 2026, acknowledging the industry’s critical condition and attempting to conceal the scale of the crisis from international observers.

Europe: Sanctions Evasion Through Energy Proxies

The Kremlin is attempting to create artificial demand for Russian oil in Europe by using friendly states. Hungary and Slovakia are pressuring Ukraine to restore Russian oil transit via the Druzhba pipeline to supply Serbia’s Naftna Industrija Srbije (NIS), which Moscow views as a strategic foothold in the Balkans.

Sanctions imposed on NIS in October 2025, due to Gazprom’s 56.15% stake, led to the shutdown of Serbia’s only refinery in Pančevo after crude supplies via Croatia’s JANAF pipeline were halted and international payments blocked, pushing Serbia toward a fuel crisis.

In January 2026, Russia blocked a $600 million acquisition offer from ADNOC for Gazprom Neft’s stake in NIS, demanding $1.2 billion instead. Under pressure, Serbian President Aleksandar Vučić agreed to transfer Gazprom Neft’s shares to Hungary’s MOL Group for $0.9–1 billion under a buyback mechanism, nominally changing ownership while preserving Russian control.

Hungary initiated changes to NIS’s charter to expand the board to 11 members, enabling MOL-aligned directors to strip Serbia of veto rights and transfer operational control to Budapest and Moscow.

OFAC approval of this deal by March 2026 would create a financial loophole, allowing sanctioned firms like Gazprom Neft and Lukoil to continue operating in Europe through intermediaries, undermining EU energy security.

These moves are synchronized with energy blackmail against Ukraine, exploiting its dependence on diesel and electricity imports. Hungary and Slovakia have threatened to halt diesel supplies covering up to 40% of Ukraine’s market, demanding unimpeded transit of Russian Urals crude via southern Druzhba.

Prime Minister Viktor Orbán’s February 2026 veto of a €90 billion EU credit for Ukraine, explicitly tied to restoring Russian oil transit, represents overt financial coercion coordinated with Moscow.

Risk Matrix for the European Union

Core risk: not the resumption of large-scale Russian oil deliveries, but the legitimization of sanctions-evasion mechanisms that transform individual EU member states into institutional proxies of the Kremlin, undermining the EU’s capacity to act as a unified geopolitical actor.

Key Strategic Message

Russia is no longer trying to win the sanctions war economically — it is trying to win it institutionally.

The Western response must focus not on new exemptions, but on closing the mechanisms that legalize sanctions evasion through allied jurisdictions.

More on this story: Sanctioning Leverage: U.S. Influence Through India’s Russian Oil Trade