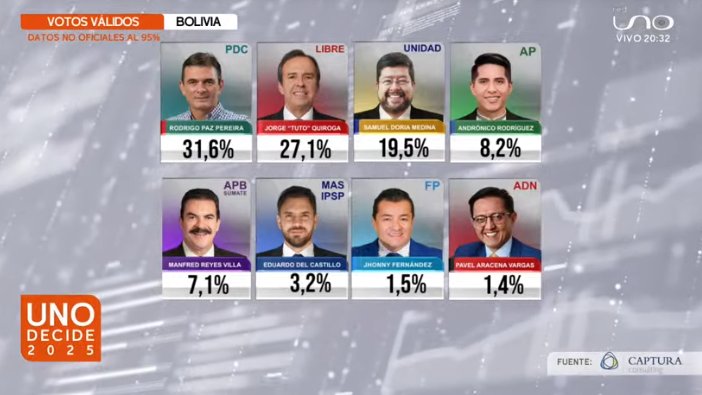

- Result so far: First round (Aug 17, 2025) points to a runoff on Oct 19 with Rodrigo Paz (centrist) versus Jorge “Tuto” Quiroga (right‑of‑center). MAS (Evo Morales/Luis Arce’s party) suffered a historic collapse amid internal schism and Morales’s exclusion from the ballot.

- Drivers: Deep economic crisis (fuel and dollar shortages), legitimacy shock after the failed June 2024 coup attempt, and fragmentation of the ruling camp.

- What’s next: The runoff will set the policy course on stabilization, lithium, and alignment with China/Russia versus a reset toward multilateral lenders and the U.S./EU.

The race leaders & vote dynamics

- Rodrigo Paz (centrist, anti‑corruption message): Surged on a reformist, inclusive‑market platform; picked up urban and swing voters; now positioned to aggregate anti‑MAS and moderate right votes. Key boost: Doria Medina signaling support after finishing behind the top two.

- Jorge “Tuto” Quiroga (right‑of‑center, ex‑president): Campaigns on sharper liberalization/privatization and external financing; strong in conservative regions and parts of the business class.

- MAS (fractured): Morales barred by the courts; Arce faction vs. “evistas” split the base; boycott calls depressed MAS turnout. Even where MAS retains municipal muscle, its national brand is at a 20‑year low.

Possible outcomes (scenarios)

- Paz wins the runoff (base case)

- Economy: Gradual stabilization (fx, fuel, debt service) with a governance/anti‑corruption frame; room for a limited IMF‑style program while keeping social spending buffers.

- Lithium: “Clean‑up and speed‑up” approach: audit opaque deals, keep partnerships but rebalance contract governance; aim to unlock midstream (carbonate/hydroxide) investment stalled by political fights.

- Foreign policy: Re‑open to EU/U.S. technical assistance while not severing China ties; more scrutiny of Russia‑linked contracts.

- Risk: Street mobilization by evista unions challenging legitimacy; short‑term labor unrest in mining/transport.

- Quiroga wins the runoff (market‑maximalist case)

- Economy: Faster liberalization—subsidy reform, privatization signals, aggressive multilateral financing—delivers quicker macro gains but higher near‑term social friction.

- Lithium: Push to re‑tender or renegotiate Chinese/Russian frameworks; prioritize Western/Japanese/Korean capital and clearer offtake terms. Expect legal disputes over contracts signed in 2023–25 (e.g., Uranium One/Russia path.

- Foreign policy: Pivot toward Washington/Brussels; ALBA ties cool.

- Risk: Higher probability of disruptive protests from MAS‑aligned sectors and coca unions; possible regional tension with Peru’s border zones if smuggling routes are hit.

- Hung parliament / contested street politics (tail‑risk overlay)

- Legislative fragmentation forces cross‑bloc bargaining on budget and hydrocarbons; reform pace slows.

- Security: Post‑coup trauma plus radicalization of factions increases blockade politics; targeted disruption at fuel/lithium nodes possible

Strategic consequences to watch

- Lithium governance as king‑maker: Congress fights over Chinese/Russian contracts already turned chaotic; a new executive will face immediate tests on transparency, revenue‑sharing with regions (Potosí/Oruro), and industrialization timelines. Expect early legislative moves on contract disclosure and royalties.

- Geopolitical rebalancing:

- If Paz/center wins: calibrated diversification—keep Chinese capital, tighten compliance, cool Russia linkages; reopen to EU Battery Alliance, U.S. IRA‑adjacent supply chains.

- If Quiroga/right wins: clearer Western tilt; legal and diplomatic friction with Moscow/Beijing over contract sanctity likely.

- MAS after defeat: From hegemon to movement‑opposition. Morales retains mobilization capacity; Arce‑litetechnocrats may try a post‑MAS centrist social‑democracy. Street pressure remains the lever.

- Institutional resilience: The swift defeat of the 2024 coup attempt raised the bar for overt military adventurism, but politicization risks linger; civil‑military management will be an early test for the next president.

Results by municipality. Source

What changes in Bolivia’s political landscape

- End of the MAS era (for now): A generational opening for centrist anti‑corruption politics and a modernized, pro‑competition right

- Regional re‑weighting: Santa Cruz business networks regain leverage in energy/logistics; Potosí/Oruro assert harder claims over lithium rents.

- Issue‑based coalitions: Less ideology, more delivery politics—inflation, fuel, jobs, and tangible progress at lithium plants will decide early approval.

- Contract politics goes mainstream: Expect litigation and congressional investigations into 2023–25 lithium deals(China/Russia) and a push for standardized, transparent templates.

Quick indicators to monitor (Aug–Nov)

- Runoff alignments: Formal endorsements (e.g., Doria Medina → Paz) and whether smaller right parties coalesce or split.

- Lithium signals: First 100‑day decrees on YLB governance, contract publishing, and midstream plant timelines.

- Stabilization plan: Any pact with multilaterals; moves on subsidies, exchange management, and fuel imports.

- Street temperature: ACLED‑tracked protests/roadblocks around Chapare/Yungas and mining corridors.

Runoff strategy matrix (Oct 19, 2025)

| Dimension | Rodrigo Paz (centrist) | Jorge “Tuto” Quiroga (right-of-center) |

| Core message | Anti-corruption, pragmatic stabilization, “50–50” state–market balance | Fiscal shock therapy, liberalization, IMF door open, “reverse 20 lost years” |

| Vote base & geography | Urban middle class; moderate/anti-MAS swing voters; gains in La Paz–Cochabamba–Santa Cruz corridors | Conservative/business vote; Santa Cruz networks; parts of Tarija/Chuquisaca provincial elites |

| Coalitions & endorsements | Public backing from Samuel Doria Medina and smaller centrist lists; likely to aggregate anti-MAS moderates | Natural magnet for harder right lists; risks splitting with centrists wary of pace of reforms |

| Turnout math (path to 50%+) | Convert Doria Medina’s voters + peel soft right in cities; keep abstention low in altiplano | Maximize Santa Cruz margins + win swing cities; suppress MAS protest vote/abstention |

| Macroeconomic line | Gradual stabilization; tighten leakages; close loss-making SOEs; targeted social buffers | Faster subsidy rollback; spending cuts; privatization signals; external financing early |

| Lithium governance | Audit & keep viable deals but raise transparency, compliance, and local rent-sharing | Re-tender/renegotiate China/Russia deals; pivot to OECD/Japan/Korea capital; legal disputes likely |

| Foreign policy | Re-balance toward EU/U.S. while keeping China ties; cooler posture toward Russia | Clearer Western tilt; ALBA distance; scrutiny of Moscow/Beijing contracts |

| Risks & counters | Union/evista street pressure; legislative fragmentation | Social backlash to rapid reforms; contract litigation; polarization hardens |

| Biggest vulnerability | Street mobilization framing him as “soft continuity” | Being cast as “privatizer/austerity,” fueling blockades/strikes |

Why this matrix: First-round results point to an Oct 19 runoff with Paz vs. Quiroga, after a historic collapse of MAS. Doria Medina has signaled support for Paz, improving Paz’s coalition math.

Lithium contract tracker — election-sensitive annex

| Deal / Counterparty | Asset / Scope | Headline terms (public) | Current status | Key friction points | If Paz wins | If Quiroga wins | Next gate(s) |

| CBC (CATL–BRUNP–CMOC) + YLB | 2 DLE plants (Uyuni); midstream LCE | ≈ $1 bncapex; ~35kt/y; YLB ~51% | Signed (Nov 2024); suspended by court (mid-2025) pending appeals | Transparency, local consultation, environmental due process; legislative approval politics | Likely review + compliance upgrades, keep timeline with stricter disclosure | Renegotiate/retender toward OECD/Japan/Korea; legal wrangling with CBC possible | Court appeals; any enabling law in new Congress; EIA sign- |

| Uranium One (Rosatom) + YLB | 1 DLE plant (Uyuni/Llipi) ~14 kt/y LCE | ≈ $970 m; YLB majority stake | Signed (Sep–Dec 2024); suspended by court (mid-2025) | Governance, geopolitics (Russia), Congress approval | High-scrutiny review; keep only if governance/ESG tightened | Probable cancellation/retender; higher dispute risk with Rosatom unit | Court appeals; legislative approval; project financing clarity |

| CITIC Guoan + YLB(smaller/pilot footprint) | Pilot/industrial plant testing (Uyuni) | Pilot-to-industrial pathway under discussion | MoUs/technical pilots reported; swept into broader court suspensions narrative | Pilot transparency; integration into national plan | Fold into unified lithium roadmap; allow pilots with strict KPIs | Pause pilots; re-open competitive tenders | Clarify tendering; publish pilot KPIs and audit trail |

What changed in 2025: Local courts in Potosí ordered suspension of major lithium contracts with CBC (CATL-led)and Uranium One (Rosatom) on transparency/consultation grounds; projects also hinge on legislative approval that stalled amid political fragmentation. Expect the next administration to either rehabilitate with stricter terms (Paz) or re-tender/pivot (Quiroga)—with litigation risk in both paths.